Matthieu Barret-Pineaux

What Are Crypto Loss Claims Actually Worth?

Published by TerraClaim · March 2026

Your Crypto Loss Amount is not what you'll recover. And right now, nobody can tell you exactly what it is worth — because half the claims in this case haven't even been processed yet. Here's what we do know, and what it means for your options.

Face Value Is Not Recovery Value

When the Plan Administrator processed your claim, they assigned a Crypto Loss Amount based on the evidence you submitted — wallet data, exchange API keys, or manual documentation. That figure represents your recognized loss. It does not represent what you'll recover.

Recovery depends on a simple formula: the total distributable pool, divided across all Allowed Crypto Loss Claims on a pro rata basis. But here's the problem — we don't know the denominator yet.

As of the Plan Administrator's Third Status Update filed February 17, 2026, only 8,449 of the 16,640 filed claims have received an Initial Determination. Of those, approximately 87% have been accepted and are now Allowed. That leaves over 8,000 claims — more than half the total — still working through the system.

Some 3,129 claims are pending Individualized Review. Another 3,760 claimants have been asked for additional information. Over 1,200 were voided as duplicates. And no Final Determinations on disputed claims have been issued yet.

Until this process is complete, nobody knows the total dollar amount of Allowed Crypto Loss Claims. You may have seen estimates floating around — figures like "$17 billion in total claimed losses." These numbers are meaningless. They conflate raw filed amounts with what will actually be Allowed, ignore the thousands of claims still under review, and pretend a denominator exists when it doesn't. Any per-dollar recovery calculation built on a guess is just math performed on fiction.

What We Do Know About the Pool

While the denominator is unknown, we know quite a bit about the numerator — the money available for distribution.

The $204 million SEC Settlement Fund, sourced from Do Kwon's settlement, is ringfenced exclusively for Crypto Loss Claim holders. This money cannot be diverted to General Unsecured Claims or absorbed by administrative costs. It represents the floor of recovery for every CLC holder, regardless of what else happens in the case.

Beyond that, the court has approved a distributable range of $185 million to $442 million from the estate's GUC Pool. But CLC holders are subordinate to General Unsecured Claims in the payment hierarchy. As we explain in detail in our guide to the distribution waterfall, GUCs get paid first and in full before any remainder flows down to CLCs. The size of those GUC obligations directly affects what's left for you.

An additional $19 million from Do Kwon's criminal forfeiture is also available, though its allocation depends on the Plan Administrator's discretion and court approval.

The Two Lawsuits That Could Change Everything

The most significant variable in the recovery picture is litigation.

The $4 billion lawsuit against Jump Trading, filed December 19, 2025, alleges that Jump entered into secret arrangements with Terraform Labs — receiving LUNA tokens at roughly $0.40 when the market price exceeded $100, and backstopping the UST peg in May 2021 without disclosure. A second lawsuit against Jane Street Group LLC was filed in February 2026 in the Southern District of New York, alleging that Jane Street used material non-public information to execute a massive UST swap that helped trigger the death spiral. An answer from Jane Street isn't due until April 27, 2026.

If even a fraction of the Jump Trading claim is recovered, the distributable pool grows dramatically. And the Jane Street case opens a second front. The Plan Administrator has also indicated that additional lawsuits against other third parties are being investigated.

These cases represent the difference between a modest recovery and a potentially transformative one. But litigation is binary and unpredictable — and could take years to resolve.

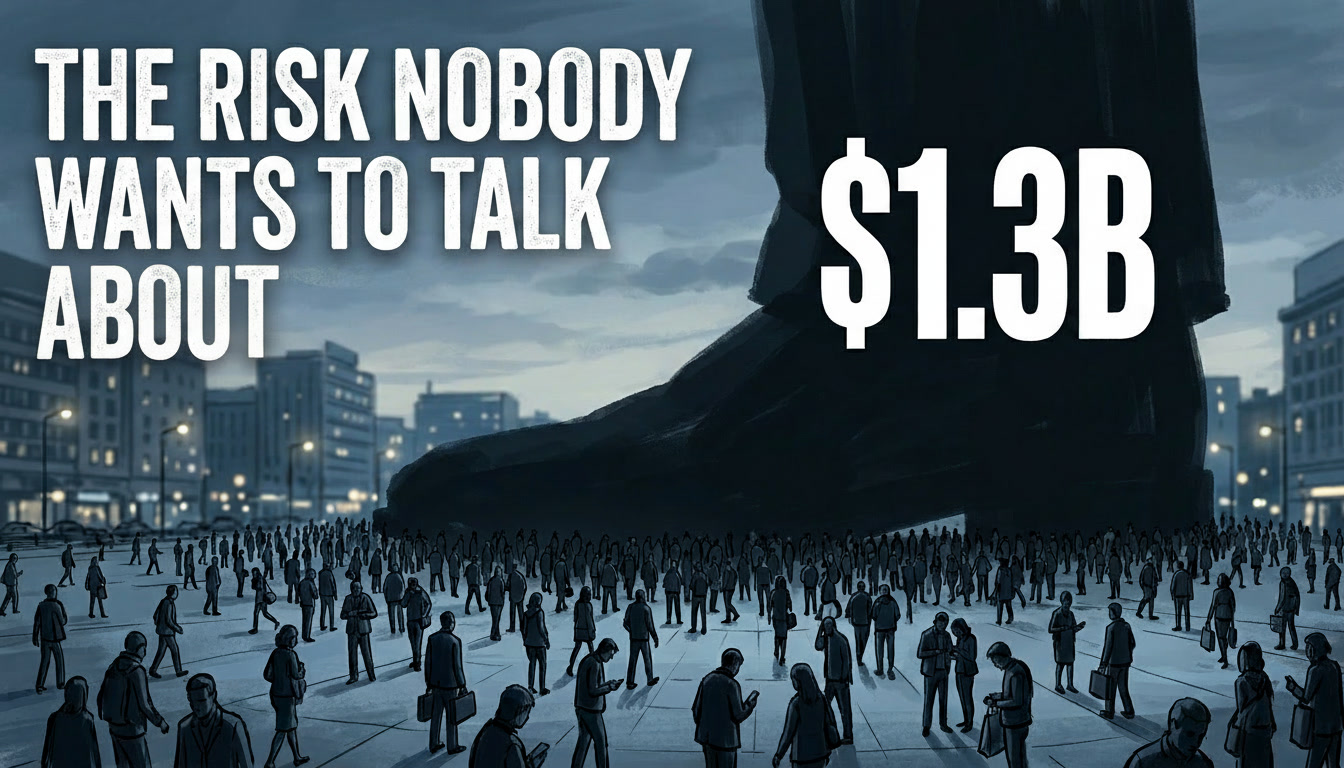

The 3AC Structural Risk

Three Arrows Capital's $1.32 billion claim was approved in October 2025 and classified as a Crypto Loss Claim. As a CLC, it sits in the same tier as every individual creditor's claim — diluting recovery but not changing priority.

If 3AC's claim were reclassified as a General Unsecured Claim, it would move to the front of the line. A $1.32 billion GUC claim would consume the entire GUC Pool, leaving zero remainder for CLC holders. In that scenario, recovery would be limited to the SEC Settlement Fund alone.

Legal counsel has assessed reclassification as essentially impossible at this stage, given that the claim has already been reviewed and approved as a CLC. But the risk, however remote, is structurally embedded in how the estate is valued by professional claim buyers.

Why Buyers Offer a Few Cents on the Dollar

The honest answer is that no one knows exactly what Terra claims are worth today — and the only way to find out what institutional buyers will actually bid is when the market goes live. What we do know is that the level of uncertainty in this case — an undetermined total CLC denominator, multibillion-dollar lawsuits still in early stages, the 3AC reclassification question, and a distribution timeline that could stretch years — means buyers cannot responsibly price claims at more than a few cents on the dollar upfront.

But upfront price is no longer the whole story. TerraClaim's recovery-sharing structure was designed precisely for this situation: a case where the floor is low but the ceiling could be multiples higher. Rather than forcing a single number onto an unknowable outcome, the structure lets buyers make a balanced offer — guaranteed cash today that reflects the current uncertainty, combined with continued seller participation in future distributions as that uncertainty resolves. The result is a deal that adjusts itself to the outcome. If the estate recovers at the floor, the seller received fair value. If litigation delivers and recovery climbs, the seller's total proceeds climb with it.

There is also the time value of money. A recovery that arrives in 2028 or 2029 is worth less in today's dollars than one that arrives tomorrow. And there is structural risk: the 3AC question, the possibility of additional administrative costs, and the general unpredictability of complex bankruptcy proceedings. The recovery-sharing mechanism accounts for all of this by letting the market price the certainty component separately from the upside component — instead of collapsing both into a single discounted number.

The FTX Precedent — And Why This Time Can Be Different

Creditors in the FTX bankruptcy saw a dynamic that Terra claim holders should study carefully but not treat as a blueprint. Early in that case, claims traded at roughly 3 to 6 cents on the dollar. As the estate recovered far more than expected, claim prices climbed dramatically, eventually approaching par value. Creditors who sold early received certainty and immediate liquidity — but gave up all exposure to the upside that followed.

The two cases, however, are fundamentally different. FTX's recovery story was driven by identifiable, recoverable assets — crypto holdings whose value surged with the market, venture investments that could be liquidated, and a relatively straightforward path from estate assets to creditor distributions. The uncertainty in FTX was primarily about price and timing. The underlying pool of assets was known early on, and once crypto markets recovered, the distribution math became clear relatively quickly. Buyers who purchased claims at 3 cents understood exactly what they were buying — they were making a directional bet on asset recovery, and the bet paid off.

Terra is a completely different situation. The uncertainty here is structural, not just directional. The total Allowed CLC denominator is still unknown. The two largest potential sources of recovery — the Jump Trading and Jane Street lawsuits — are litigation outcomes, not existing assets waiting to be sold. Whether they produce $0 or billions depends on court rulings that could take years. The 3AC reclassification question could reshape the entire waterfall overnight. And the Plan Administrator is still processing thousands of claims through Individualized Review. There is no single asset to watch, no market price to track, no moment where the picture suddenly becomes clear. The uncertainty is layered, multi-dimensional, and will resolve gradually over years.

That is precisely why TerraClaim's recovery-sharing structure matters more here than it would have in FTX. In a case like FTX, a flat sale was a clean bet — you were either right or wrong about asset values, and the answer came relatively fast. In Terra, a flat sale forces a single price onto a set of outcomes so wide and so slow to resolve that any fixed number is almost guaranteed to be wrong in one direction or the other. The recovery-sharing mechanism was designed for exactly this kind of case: one where the floor is knowable but the ceiling depends on litigation, reclassification rulings, and administrative decisions that will play out over years. Instead of collapsing all of that into a single discounted price, the structure lets the deal adjust itself as the uncertainty resolves.

A seller who transacts today at a few cents on the dollar still receives additional payments if the estate recovers 15%, 20%, or 25% — automatically, contractually, with no further action required. The lesson from FTX is not that selling early was wrong. For many creditors, the certainty and liquidity were worth it. The lesson is that the market lacked a mechanism to let sellers capture both. That mechanism now exists — and it was built specifically for cases like Terra, where the range of outcomes is wide, the timeline is long, and no one can honestly tell you today what your claim will ultimately be worth.

The fundamental question is the same one FTX creditors faced: what is certainty worth to you? But for the first time, the answer doesn't have to be all or nothing.

You Deserve to Understand the Structure

We write this as creditors ourselves — TerraClaim's founders hold Crypto Loss Claims in the Terraform Labs bankruptcy. And we know from experience that the hardest part of this process is not the legal complexity or the waiting. It is making decisions without knowing the full picture. The total Allowed CLC amount has not been determined. Two multibillion-dollar lawsuits are pending. A $1.32 billion claim from 3AC introduces structural risk. And the Plan Administrator is still working through thousands of claims in Individualized Review. No one can tell you with certainty what your future distribution will be — and anyone presenting a precise figure is working from assumptions, not facts.

What we can tell you is that you deserve to understand the structure. You deserve to know where the money comes from, how the waterfall works, what the lawsuits mean, and what options are available on the secondary market — so you can make a decision based on your own circumstances, not someone else's assumptions.

If you want to learn more, TerraClaim is here to help. No seller fees. No pressure. Just the information you need to decide what is right for you.

This is not legal or financial advice. Consult a qualified professional before making decisions about your claim.