Matthieu Barret-Pineaux

Understanding the Terra Bankruptcy Distribution Waterfall

Published by TerraClaim · March 2026

If you hold a Crypto Loss Claim in the Terraform Labs bankruptcy, the most important thing you can understand is how money moves from the estate to your pocket. The distribution waterfall — the legally defined order in which creditors get paid — determines not just whether you receive a terra luna bankruptcy payout, but how much and when. This guide is our definitive breakdown of the Terraform Labs distribution waterfall and the CLC distribution order, written for creditors who want to understand the actual mechanics behind the numbers.

What a Distribution Waterfall Is

In any bankruptcy, not all creditors are equal. The law establishes a priority system that dictates who gets paid first. Higher-priority claims are satisfied before lower-priority ones. If the money runs out before reaching your tier, you may receive a reduced distribution or nothing at all. This priority system is called the distribution waterfall because funds flow from the top — the estate's available assets — down through successive tiers of creditors until the pool is exhausted.

In the Terraform Labs case, Case No. 24-10070 in the U.S. Bankruptcy Court for the District of Delaware, the waterfall has several distinct layers, and where your claim sits in that structure is the single biggest factor in your expected recovery.

Before the Waterfall Begins: Administrative Costs

Before a single dollar flows to any creditor — whether General Unsecured or Crypto Loss — the estate must pay its administrative expenses. In bankruptcy, this means the law firms, financial advisors, claims agents, and other professionals retained to run the case. These costs are not optional. Under the Bankruptcy Code, they are paid in full from estate assets ahead of every other class of creditor.

In the Terraform Labs case, these costs are substantial. Court filings show that Dentons US LLP, the special litigation counsel retained to defend Terraform in the SEC enforcement action, received final approval for approximately $24.6 million in fees and expenses for roughly eight months of work during the case. McDermott Will & Emery, counsel to the Official Committee of Unsecured Creditors, was approved for approximately $9.1 million. A separate fee application from Genesis Credit Partners, the Committee's co-financial advisor, drew formal objections from the U.S. Trustee over billing irregularities and remains contested. These three firms alone account for over $34 million in confirmed or requested fees — and they are not the only professionals in the case. Lead bankruptcy counsel Weil, Gotshal & —Manges, financial advisor Alvarez & Marsal, local Delaware counsel Richards, Layton & Finger, and claims agents Epiq and Kroll all filed their own fee applications, the details of which are available only through the court's PACER system.

After the Plan's Effective Date on October 1, 2024, a new layer of professional costs began. Kirkland & Ellis and Reid Collins & Tsai now represent the Plan Administrator in the Jump Trading and Jane Street lawsuits, and their fees — along with those of the Plan Administrator and claims agent Kroll — are paid from estate assets in the ordinary course, without requiring further court approval. These post-confirmation costs are not publicly reported.

The total administrative burden is difficult to quantify precisely, but based on confirmed data and comparable crypto bankruptcy cases, pre-confirmation professional fees alone likely fall in the range of $55 million to $80 million. Against a GUC Pool estimated at $185 million to $442 million, that is not a rounding error — it is a meaningful reduction in the funds available to flow down the waterfall to creditors. The SEC Settlement Fund, discussed below, is ringfenced and protected from these costs. But the GUC Pool is not. Every dollar spent on administration is a dollar that does not reach General Unsecured Claims or Crypto Loss Claims.

This is the layer most creditors never hear about — and it is the first claim on every dollar the estate holds.

Layer One: The SEC Settlement Fund ($204 Million)

At the top of the waterfall — or more accurately, separate from it — is the $204 million SEC Settlement Fund. This money comes from Do Kwon's settlement with the Securities and Exchange Commission and is ringfenced exclusively for Crypto Loss Claim holders. It cannot be diverted to General Unsecured Claims. It cannot be absorbed by administrative costs. It is reserved specifically for CLC distributions.

This $204 million represents the absolute floor of recovery for creditors who filed Crypto Loss Claims. Regardless of what happens with the GUC Pool, regardless of litigation outcomes, regardless of the 3AC reclassification risk we discuss below, this money is reserved for your claim class. How much that translates to per dollar of claimed loss depends on the total Allowed CLC amount, which is still being determined as thousands of claims work through Individualized Review. What is certain is that the money exists and is ringfenced.

An additional $19 million from Do Kwon's criminal forfeiture is also available to the estate, though its precise allocation within the waterfall depends on the Plan Administrator's discretion and court approval.

Layer Two: The GUC Pool — Where the CLC Distribution Order Matters Most

The second major source of recovery is the GUC Pool — the general estate funds available for distribution. The court has approved a distributable range of $185 million to $442 million from this pool.

Here is where the waterfall's priority structure becomes critical for understanding your terra luna bankruptcy payout: General Unsecured Claims get paid first. In full. Before any money from the GUC Pool reaches Crypto Loss Claim holders, every GUC must be satisfied dollar for dollar. Only the remainder — whatever is left after all GUC obligations are met — flows down to CLCs on a pro rata basis.

This is the subordination that most creditors don't fully understand. Your Crypto Loss Claim is not equal to a General Unsecured Claim. It is behind it. If the GUC Pool is $400 million and GUC obligations total $100 million, then $300 million flows to CLCs. But if GUC obligations are higher, the CLC share shrinks accordingly.

This subordination is also why upfront purchase rates on the secondary market are measured in cents, not dollars — buyers cannot price claims higher than the floor justifies until the uncertainty above it resolves. TerraClaim's recovery-sharing mechanism addresses this directly: instead of compressing the entire waterfall into a single discounted price, it lets sellers receive cash today for the certainty component and retain participation in the layers above as they play out.

The Three Arrows Capital Risk in Waterfall Context

This is where the 3AC issue becomes critical to the distribution waterfall mechanics.

Three Arrows Capital's $1.32 billion claim was approved in October 2025 and classified as a Crypto Loss Claim. As a CLC, it sits in the same tier as every other individual creditor's claim. It dilutes recoveries, but it doesn't change the priority structure.

If 3AC's claim were reclassified as a General Unsecured Claim, it would move to the front of the line. A $1.32 billion GUC claim would consume the entire GUC Pool and then some, leaving zero remainder to flow down to CLCs. In that scenario, creditors would be limited to the $204 million SEC Settlement Fund — spread across a total Allowed CLC amount that has not yet been determined.

Reclassification of the full 3AC claim is considered very unlikely given that it has already been reviewed and approved as a CLC. However, the possibility that some portion of the claim could be requalified has not been ruled out. The risk, even if remote, is structurally embedded in the waterfall and affects how the entire estate is valued by professional claim buyers.

Layer Three: Litigation Proceeds — The Potential to Transform Recovery

The third and potentially largest source of recovery comes from pending lawsuits filed by the Terraform Wind Down Trust.

The $4 billion lawsuit against Jump Trading, filed December 19, 2025, in the Northern District of Illinois, alleges that Jump entered into secret arrangements with Terraform Labs, received LUNA at deeply discounted prices, backstopped the UST peg without disclosure, and profited roughly $1 billion while retail investors lost approximately $40 billion. Jump's subsidiary Tai Mo Shan has already paid $123 million in an SEC settlement.

The lawsuit against Jane Street Group LLC, filed in February 2026 in the Southern District of New York under Case No. 1:2026-cv-01536, alleges manipulative trading activity during the collapse. As we analyzed in our coverage of the Jane Street lawsuit, this case adds a second independent litigation catalyst to the recovery picture, with an answer due from Jane Street by April 27, 2026.

Any proceeds from these lawsuits would flow into the estate and through the same waterfall: GUCs first, then CLCs. The sheer scale of the amounts claimed — $4 billion against Jump alone, plus an undisclosed amount against Jane Street — means that even a partial recovery from litigation could dramatically increase the total distributable pool. The exact impact on per-dollar recovery depends on both the litigation outcomes and the total Allowed CLC amount, neither of which is known today.

For creditors considering a sale, this is the layer that matters most in evaluating their options. Litigation proceeds are the highest-variance component of the waterfall — potentially transformative, but years away and uncertain. TerraClaim's recovery-sharing structure ensures that sellers who transact today still participate in this layer if it delivers. You do not have to choose between liquidity now and litigation upside later.

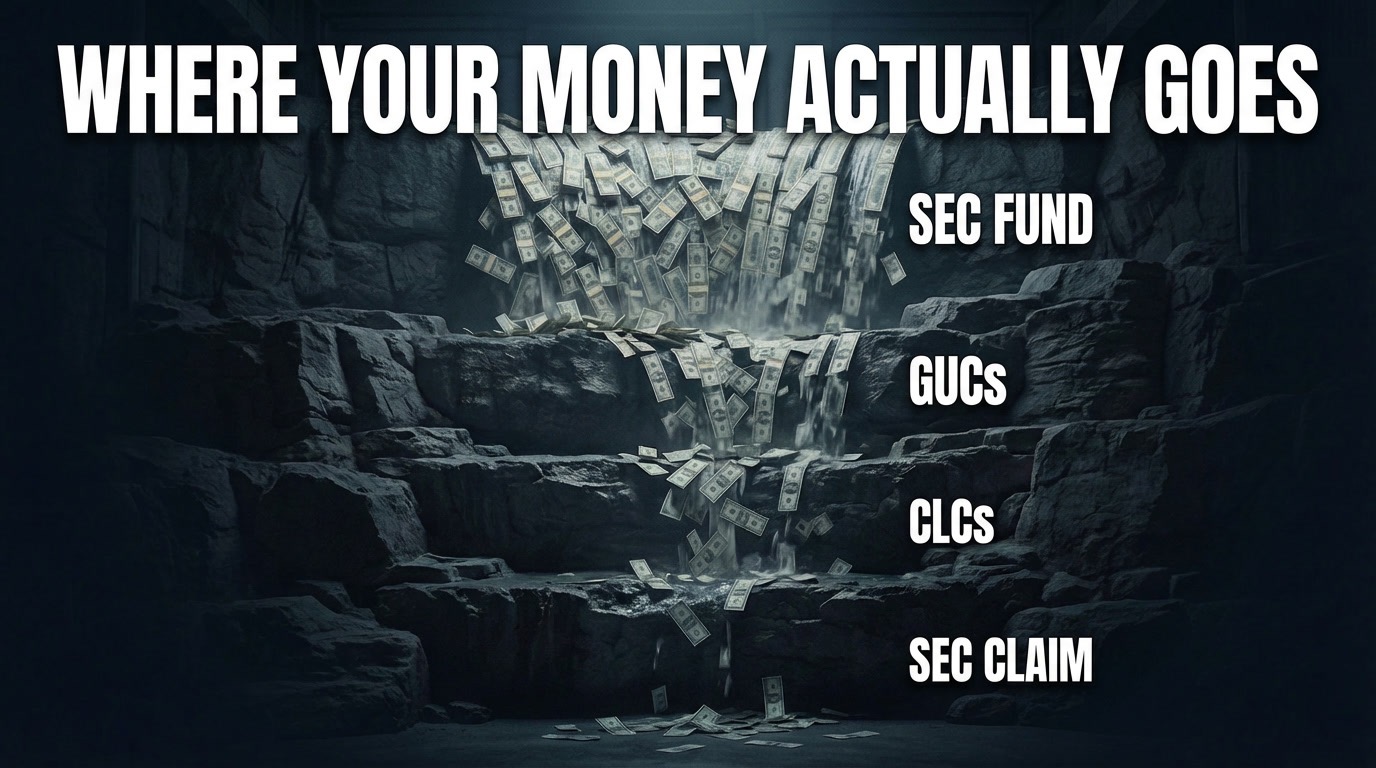

The Full Terraform Labs Distribution Waterfall at a Glance

The distribution waterfall for Terra creditors works in this order. First, administrative expense claims — the professional fees discussed above — are paid from general estate assets. Second, the $204 million SEC Settlement Fund pays CLCs directly — this is ringfenced and guaranteed for your claim class. Third, the GUC Pool distributes to General Unsecured Claims in full. Fourth, whatever remains in the GUC Pool after GUC satisfaction flows to CLC holders pro rata. Fifth, proceeds from the Jump Trading and Jane Street lawsuits, if successful, enter the estate and flow through the same GUC-first-then-CLC structure.

The range of possible recovery outcomes — from modest to potentially transformative — flows directly from this waterfall. As we laid out in our breakdown of what crypto loss claims are actually worth, the range depends entirely on how much enters each layer, how much makes it through to CLCs after senior obligations are met, and the total Allowed CLC denominator — which has not yet been determined.

What This Means for Your Payout Decision

Understanding the distribution waterfall is not an academic exercise. It directly informs how you think about your claim — and it's the reason TerraClaim built a recovery-sharing mechanism specifically adapted to this case's structure.

The waterfall tells you that the SEC fund provides a guaranteed floor (though the per-dollar amount depends on the final denominator), that the base case depends heavily on the GUC Pool remainder after senior obligations are met, and that successful litigation against Jump Trading and Jane Street could push the total distributable pool dramatically higher. That is an unusually wide range of outcomes — and it is precisely what makes a flat sale at a few cents on the dollar such a difficult decision. You'd be pricing an unknowable ceiling into a single number.

Because the Terra case has this unique profile — a low floor driven by existing estate assets, but significant upside tied to ongoing litigation — TerraClaim's legal and technical team developed a recovery-sharing mechanism specifically adapted to this market. Instead of a flat purchase at a few cents on the dollar, every trade on TerraClaim guarantees you cash at closing — and on claims of $100k and above, a built-in structure continues to pay you a share of future distributions as the estate recovers funds.

If the GUC Pool delivers a strong remainder, you benefit. If the lawsuits succeed and litigation proceeds enter the estate, you benefit from that too. The structure adjusts itself to the actual outcome rather than forcing you to bet on a single scenario today.

Every creditor's situation is different. Your claim size, your financial needs, your tolerance for waiting years, and your view on litigation risk are all personal factors that no article can assess for you. Whether you choose to hold and wait, or sell with continued upside participation, the most important thing is understanding the waterfall that governs your recovery — because that is what every number, every offer, and every decision ultimately depends on.

If you want to learn more about your options, TerraClaim is here to help. No seller fees. No pressure. Just the information you need to decide what is right for you.

This is not legal or financial advice. Consult a qualified professional before making decisions about your claim. Case information is sourced from public filings in In re Terraform Labs Pte. Ltd. (Case No. 24-10070-BLS, D. Del.), the Plan Administrator's Third Status Update (Docket 1177), and related litigation dockets.

Track all case developments: TerraClaim Case Timeline